(Global energy crisis is ‘the mother of all crises’: Turkish energy minister)

As most OECD economies were entering a post-inflationary phase, the Iran war and Hormuz disruptions have reversed the trajectory. Yet the real story is not the shock itself, but how unevenly it is being absorbed. Türkiye, already fragile, is now sharply diverging from the rest of the OECD.

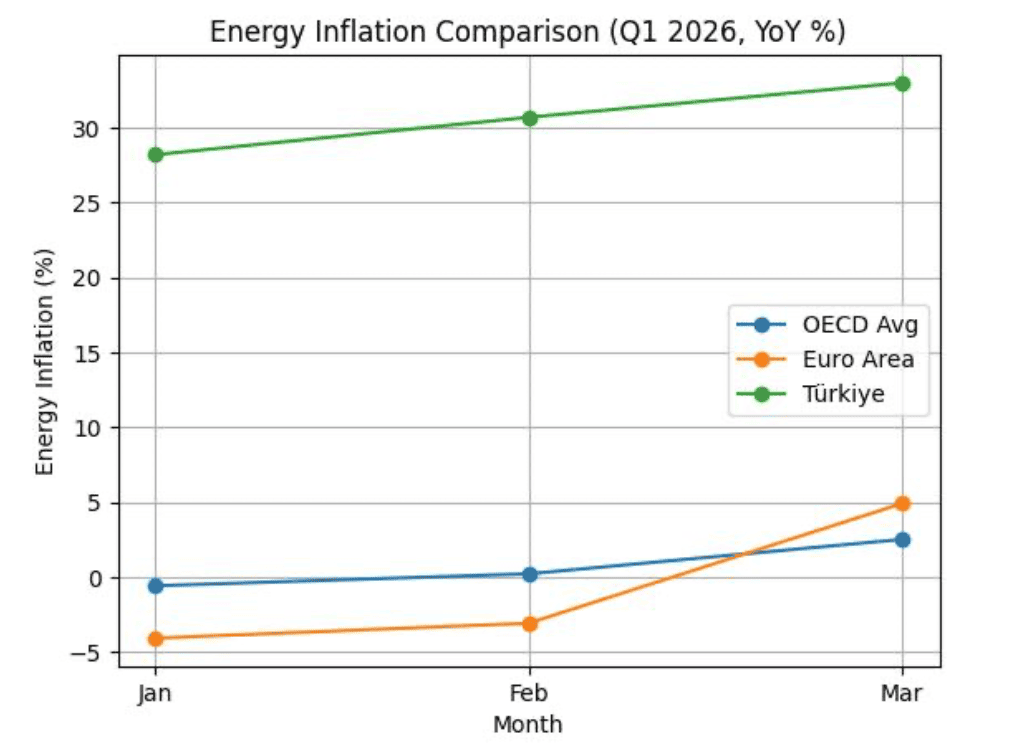

In early 2026, the global inflation narrative appeared to be turning a corner. Across the OECD, energy prices were easing, headline inflation was stabilizing, and policymakers cautiously embraced the idea of a “soft landing.” January’s figures even showed energy inflation slipping into negative territory at -0.6 percent, a symbolic milestone after years of persistent price pressures.

That narrative did not last.

By late March, escalating tensions linked to the Iran war and growing uncertainty around the Strait of Hormuz triggered what the OECD itself described as a “Hormuz shock.” Oil prices surged past the psychologically critical $100 threshold, briefly exceeding $118 per barrel, while natural gas benchmarks spiked sharply across Europe. Energy inflation in the euro area swung dramatically, from -3.1 percent in February to nearly 4.9 percent within weeks.

Yet even as this shock rippled through advanced economies, a deeper structural divergence became unmistakable. Türkiye was not merely affected. It was exposed.

A post-inflation world interrupted

For most OECD countries, the renewed energy volatility represents a setback rather than a systemic break. Inflation had been moderating steadily through late 2025 and early 2026, supported by easing supply chains, tighter monetary policy, and stabilizing commodity prices.

Even after the March escalation, the broader OECD picture remains one of relative resilience. Headline inflation hovered around 3.4 percent in February, with 16 member states already at or below the 2 percent threshold. Governments, learning from previous crises, moved quickly. By early April, at least 26 OECD countries had introduced fresh relief measures, ranging from targeted subsidies to temporary tax cuts, aimed at cushioning households from the renewed energy spike.

In other words, while the shock is real, the system is absorbing it.

Türkiye: From outlier to case study

Türkiye presents a fundamentally different picture. Even before the latest escalation, inflation dynamics in the country had already diverged sharply from OECD norms. Energy inflation stood at approximately 28 percent in January, compared to the OECD average of -0.6 percent. Headline inflation exceeded 30 percent in February, nearly ten times the OECD average.

This gap is not merely quantitative. It is structural.

As a major energy importer, Türkiye is acutely sensitive to external price shocks. Energy imports account for an estimated 3.5 to 4.5 percent of GDP, creating a direct transmission channel from global commodity prices to domestic inflation. Every sustained increase in oil prices translates quickly into higher production costs, widening current account deficits, and renewed pressure on the currency.

The April 4 tariff adjustments underscore the scale of the challenge. Electricity and natural gas prices for households were raised by 25 percent, while industrial users faced increases of up to 18.6 percent for gas and nearly 6 percent for electricity. Agricultural electricity tariffs surged by almost 25 percent, raising concerns about a second-round effect on food inflation.

Unlike many OECD peers, Türkiye is not insulating consumers from the shock. It is passing it through.

The limits of subsidy economics

This policy shift reflects a deeper constraint: fiscal sustainability.

For several years, Türkiye relied on extensive energy subsidies to contain inflationary pressures and shield households. However, as global prices rise and domestic imbalances persist, maintaining these subsidies has become increasingly costly. The April tariff hikes signal a recalibration, if not a partial retreat.

This stands in stark contrast to the broader OECD response. While Türkiye is scaling back implicit subsidies through price adjustments, many OECD governments are reintroducing support mechanisms to dampen the impact of the new energy cycle.

The divergence is therefore not just economic, but strategic.

Decoupling in real time

The result is a clear decoupling. While most OECD economies are experiencing a cyclical uptick in energy inflation following a period of decline, Türkiye appears to be entering a new inflationary cycle altogether. The OECD has already revised Türkiye’s 2026 inflation forecast upward to 26.7 percent, citing both the Hormuz shock and ongoing currency volatility.

More tellingly, Türkiye’s energy inflation is not only higher than the OECD average. It is multiple times higher than the second-highest country in the group. In a context where many economies are still managing single-digit energy inflation, Türkiye’s trajectory stands apart.

This raises a critical question. If the same global shock produces such different outcomes, how much of the divergence is external, and how much is domestic?

Beyond prices: Structural pressures build

The answer lies partly in policy design.

Türkiye’s evolving tariff structure, including the expansion of tiered pricing mechanisms, is reshaping how energy costs are distributed across households and sectors. While intended to target subsidies more efficiently, these systems can amplify price pressures for certain user groups, particularly in centrally heated buildings or high-consumption households.

At the same time, the broader macroeconomic environment compounds the challenge. Currency volatility, high inflation expectations, and limited fiscal space reduce the effectiveness of policy responses. Energy prices do not operate in isolation. They interact with wages, food prices, and production costs, creating a feedback loop that is difficult to contain.

The risk is not simply higher inflation. It is entrenched inflation.

The next phase: A new energy reality

Looking ahead, the trajectory of global energy markets will remain closely tied to geopolitical developments. The Strait of Hormuz, through which a significant share of global oil supply passes, has reemerged as a critical chokepoint. Any sustained disruption could prolong the current price cycle, delaying the return to disinflation across the OECD.

For most economies, this would mean a slower normalization. For Türkiye, it could mean something more profound: a transition into a structurally higher inflation regime driven by energy costs.

A divergence that matters

The emerging picture is therefore not one of uniform crisis, but of differentiated impact.

The OECD is experiencing a shock within a stabilizing system. Türkiye is confronting a shock within an already strained one.

This distinction matters because it shapes policy options. Countries operating within a stable framework can afford temporary interventions. Those outside it face harder choices between fiscal discipline, price stability, and social protection.

As the global energy landscape shifts once again, Türkiye’s position at the intersection of external vulnerability and internal constraint makes it not just an outlier, but a case study in how shocks propagate unevenly in an increasingly fragmented economic order.